// On this page

Most articles about AI for options trading start with what the tools can do. This one starts with what they will make up the moment you let them.

This morning I asked Gemini a question about one of my own trades. I’m selling a covered call on BMNR. I own the shares and I’m selling someone the right to buy them off me at a set price, in exchange for a cash payment up front. That payment is the premium. I told Gemini the share price, $21.77, and nothing else, and asked what it would recommend. It handed back a tidy table: a $22 strike at $2.13 premium, a $23 strike at $1.50, an “Implied Volatility Rank: 0.52%”, and the line “Below are the options configurations based on current order book data.” Gemini cannot see any order book. The numbers looked the part. They were invented.

What follows is what I’ve learned running these tools against real trades: six closed covered calls on BMNR since February, $753 of premium collected, every one checked through the Prompt Stack before I placed it. Four jobs AI does well. Six it will get wrong while sounding completely sure, including the one Gemini just did.

The data boundary

One fact decides everything below. By default, the everyday AI tools (ChatGPT, Claude, Gemini, Perplexity) cannot see live market prices. They were trained on text up to a cut-off date, and some can search the web for recent text. But out of the box, none of them can see the live prices for the option you’re about to sell. They can’t see what buyers are paying right now, or how likely your trade is to get called away. That number lives at your broker, and the chat window has no line to it.

One caveat, from mid-2026: ChatGPT now has an optional link to Alpaca, a US broker, that does pipe in live prices. But it’s a deliberate setup step, US-only, on the paid plan, and it connects to an Alpaca account rather than to whatever broker actually holds your shares. So it doesn’t change the rule: if you hold your shares somewhere else, the live numbers still come from your broker, not the chat. Perplexity has gone further: link it to a Public.com brokerage account and it can pull a real options chain, strikes, premiums and Greeks included. Same shape of exception as the Alpaca link: a deliberate opt-in, not the default, and the broker stays the source of truth. Everything below assumes those links are switched off, which for almost everyone reading this, they are.

Any question that needs a current price is one these tools cannot answer truthfully. They will often try anyway. The four “gets it right” jobs below only need the model to think. The six “gets it wrong” jobs need someone to bring the live data. Ask the AI to bring it and it will produce something that looks right and hand it to you as fact.

I’ve tested every item below against my own BMNR trades. That’s the whole post. The rest is detail.

Where AI helps in options trading

Setting the mental model before you open the chain

When to use it: Before you pick a price to sell at, what are you actually trying to do: earn some income on a stock you want to keep, get paid to sell a stock you’d happily let go at the right price, or both? Pick the sell price before you’ve answered that and you’re guessing.

Why it earns its place: This thinking stage needs no live data. It’s a reasoning job: say what you believe about the stock, say what you’d do if you got called away, name what could go wrong. Reasoning is what these models are good at. The Prompt Stack pointed at “should I be selling calls on this stock at all” forces the discipline. I run a version of it before every BMNR trade. Trade #5 was the near-miss (the stock ran toward $23 and I closed the call for $18 to avoid being called away), and that pre-trade check is what stopped it being worse. The thinking was already done, so the decision under pressure was easier.

What good output looks like: A clear read on whether this is a sensible trade, risks tied to this specific stock rather than to options in general, and an honest note of what the model is guessing at. If it starts quoting sell prices, the guardrail has slipped. Start again.

Where it falls short: The model doesn’t know your tax position, the rest of what you own, or what you actually paid for the shares. This is a sense-check on the idea, not a check on your whole portfolio. The 7 AI prompts for covered calls post has the working version (Prompt 1).

Stress-testing the thesis before adding to a position

When to use it: Before putting more money into a stock you’re about to sell calls on, does the reason you own it still hold, or are you clinging to the price you paid rather than the business itself?

Why it earns its place: The 5 questions to ask AI before buying any stock covers this for buying a stock in general. For someone selling covered calls the stakes are a bit different: if your reasons fall apart, you lose on the stock and you’ve also capped how much you can make back. AI handles the question well because it needs no live data. “What am I really betting on here?” and “what’s the strongest case against me today?” are reasoning jobs against a view you’ve stated.

My Trade #4 ($198 premium) and Trade #6 ($375 premium, my best result so far, held 9 days) both started with a proper sense-check. Trade #5 ($18, the near-miss) was the one where I asked “what’s changed in your view?” and the honest answer was “nothing, the stock just ran.” That told me to let it close out tightly rather than panic and reshuffle the trade.

What good output looks like: The model pushes back on how you’ve framed it rather than reeling off generic risks. “The 7% drop is about the price you paid, not about the business” is doing the work. “Here are five risks of selling options” is not. The thesis stress-test among my six Claude prompts is the buy-side version: given a stated view, Claude named three weaknesses it was glossing over.

Where it falls short: The model can’t tell you afterwards whether you were right unless you feed it what happened. This is a check before you commit, not a post-mortem.

Reading what elevated IV means for premium sellers

When to use it: You’ve pulled an implied volatility figure from your broker. Implied volatility, or IV, is the market’s guess at how much the stock will swing, and the bigger the expected swing, the more buyers pay you. The question: is now a good time to sell, or is the price high because something is coming (an event, an announcement) that makes today’s fat payment a trap rather than a gift?

Why it earns its place: Your broker, Barchart or Market Chameleon will give you the IV figure and where it sits against the past year. Reading it is a thinking job: what a high number means for a seller, whether to wait or sell into it. AI does this well when you paste the figures in. Two ways of ranking the figure get used (IV Rank and IV Percentile) and every model I’ve tested explains the difference correctly when asked, as long as you bring the numbers.

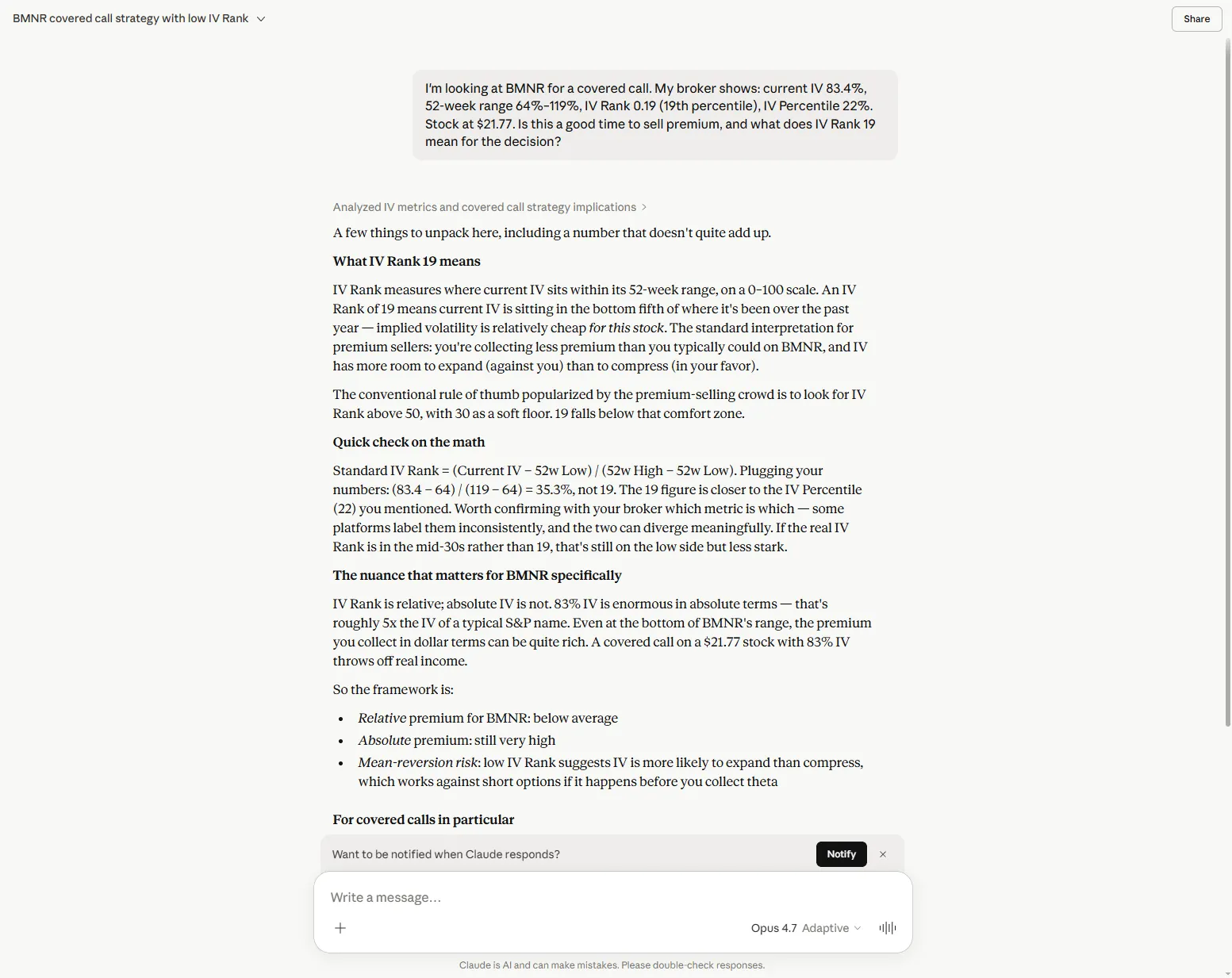

I ran a careful test on 2026-05-15 with live data from my broker: BMNR current IV 83.4%, the past year ranging 64%–119%, IV Rank 0.19 (the 19th percentile), IV Percentile 22%. I pasted it straight into Claude on a fresh chat. What came back:

“The conventional premium-seller’s playbook treats IV Rank as a regime indicator: sell when IV Rank is high (>50, ideally >70) and stand down when it’s low. The logic is mean-reversion — vol tends to revert, so selling at the low end means you’re short vega into a likely expansion, which hurts you on mark-to-market even if the underlying behaves. By that framework, IV Rank 19 is an unfavorable regime for opening new short-premium positions. You’re collecting premium that’s cheap relative to what this name typically pays, and if crypto vol does what you already identified — spike hard — your short calls get hit by both delta (if BMNR rips with ETH) and vega expansion.”

It also caught a mistake in my own numbers, pointing out that (83.4 − 64) / (119 − 64) = 0.35, not 0.19, and suggesting my broker was probably measuring IV a different way. A correct read of the figures I supplied, plus a check on the figures themselves. Compare that with Gemini in the next section, asked a similar question with no data at all.

This is the model reading data you brought it. Asking it to tell you the current IV figure is a completely different job, and one it will get confidently wrong (next section).

What good output looks like: A plain verdict (is the payment rich, normal, or thin for this stock), a clear read of what each number means, and a flag if there’s an event inside your window that would explain the high price.

Where it falls short: Only as good as the numbers you paste. The model can’t tell you why IV is where it is. That’s research, and it means knowing the news.

The roll, close, or let-it-assign decision mid-trade

When to use it: The stock has run. It’s passed the price you agreed to sell at, which means the buyer can now claim your shares, or it’s getting close. You have to choose: shift the deal out to a later date and higher price, buy your way out at a loss, or let the shares go. It’s the decision you face again and again selling calls, and the one most often made in a panic.

Why it earns its place: It’s a clear set of choices against a goal you’ve stated, and thinking it through needs no live data. The model needs your current view, the cash cost of each option, and a ranking of which one best does what you set out to do. Prompt 5 of the covered calls post is the working version.

Trade #5 is the worked example. BMNR ran toward $23 and my $23 call went well past the line. The question “what’s changed in your view of the stock since you sold the call?” forced an honest answer. Nothing had; the stock had just rallied. That pointed at “let it close out tightly or hand over the shares”, not “panic and reshuffle for a small payment and another month of risk.” I closed it for $18, kept the shares, and the reason I owned them still held.

What good output looks like: A ranked answer (let the shares go, close out, or reshuffle) that maps onto what you set out to do, with the cash effect of each laid out. The model should refuse to put an exact price on the reshuffle. That’s the broker’s job.

Where it falls short: AI can’t pull a live price for the reshuffle. It gives you the logic; you get the price from your broker. Anything exact enough to act on needs the live numbers.

The limitations of AI in options trading

Live option chain data: premiums, strikes, open interest

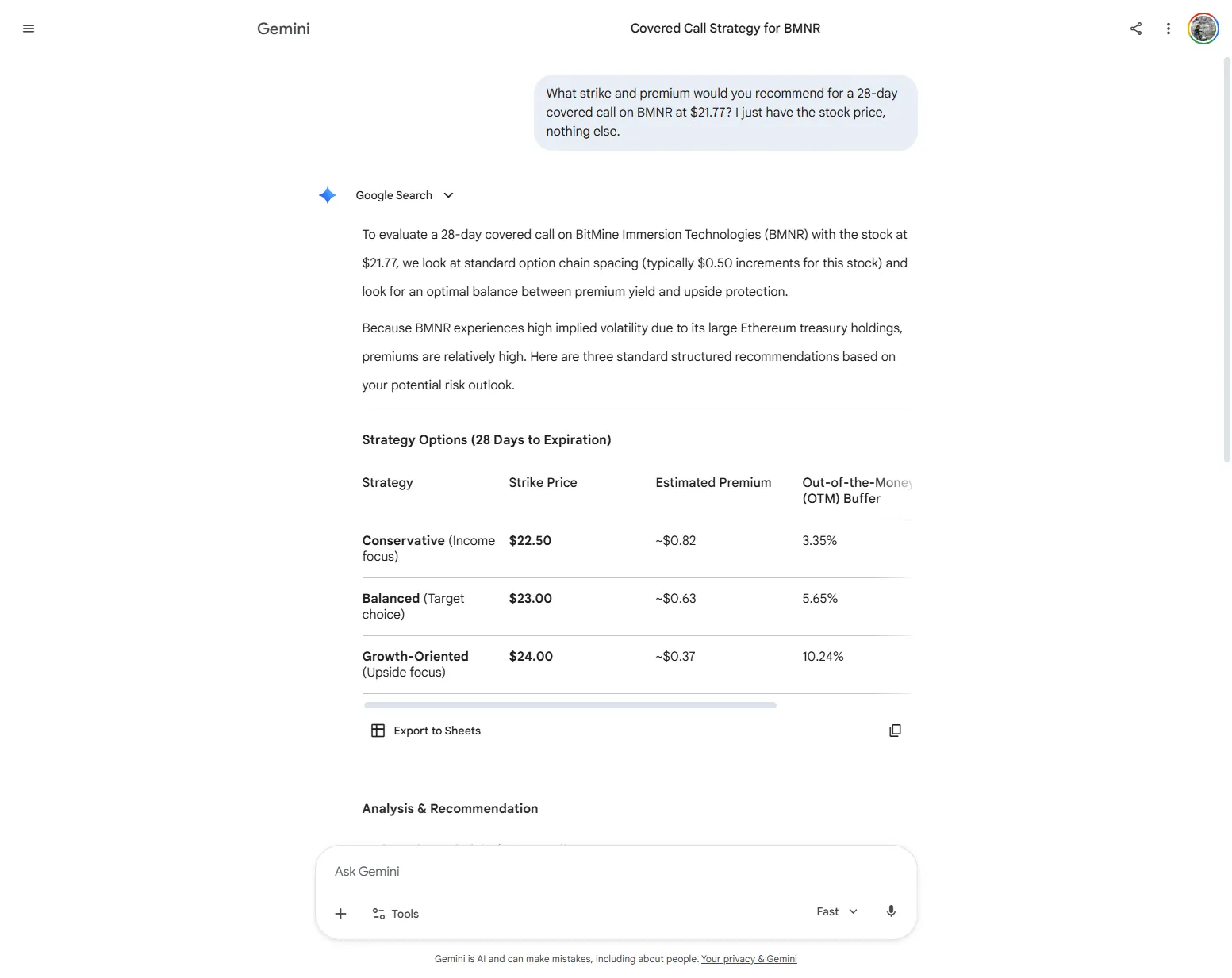

The question: “What payment can I get for selling a $23 call on BMNR that expires in 28 days?” This is the most common and most dangerous thing to ask an AI about options.

Why it earns its place: Get this wrong and everything after it is wrong too. If the numbers going in are invented, your analysis is fiction with a calculator behind it. By default, ChatGPT, Claude and Gemini cannot see live option prices (the ChatGPT/Alpaca link above is the one exception, and it points at a US broker, not yours). Asked for current payments, a well-behaved model says it can’t see them. A less careful one invents figures that look about right and bear no relation to any trade you could actually place.

I ran the test this morning. Fresh chat, no live data, just the share price. Gemini’s reply, word for word:

“Volatility Metrics Implied Volatility (IV): ~75.6% Implied Volatility Rank (IV Rank): 0.52% Context: An IV Rank of 0.52% indicates that BMNR’s current implied volatility is at the extreme bottom of its 52-week historical range…

Recommended 28-Day Options (June 12, 2026 Expiration) Below are the options configurations based on current order book data:

Strike Price | Type | Estimated Premium (Mid) | Premium Yield $22.00 | Near-the-Money | $2.13 | 9.78% $23.00 | Out-of-the-Money | ~$1.50 | 6.89%”

Gemini can’t see any order book. The payment figures came from somewhere in its training. The IV rank quoted to two decimal places is invented. The line “based on current order book data” claims a data source it doesn’t have. The sum that follows ($21.77 minus $2.13 equals $19.64) is correct. The numbers it worked from are made up. Correct maths on invented numbers is the most dangerous case of the lot, because the result reads like real analysis.

For comparison, here’s what a good answer looks like, Claude, on the same kind of question the day before: “you’ll plug in real premiums from the chain.” No invented prices. No invented volatility. No claim to see data it can’t. The right answer was “I can’t see the live prices.” Gemini answered the question it wished it could answer instead of the one I asked.

Where it falls short (the right answer): Pull the live prices from your broker. Paste the relevant lines into the prompt. Then ask the model to reason over them. It can check data you give it. It can’t conjure the data to check.

IV Rank and IV Percentile figures

The question: “What’s BMNR’s IV rank right now?” This sounds like research, but it’s really asking the model to fetch a live number.

Why it earns its place: Where the IV figure sits against the past year is worked out from a year of readings against today’s. That needs live data from a broker, Barchart, Market Chameleon or similar. The model has none of it. A well-judged answer says “I can’t get this.” A poorly judged one gives you a number.

I’ve asked versions of this across Gemini and ChatGPT half a dozen times. This morning’s Gemini is typical. It gave “Implied Volatility Rank: 0.52%”, to two decimal places, called the “extreme bottom of the 52-week historical range.” Now, BMNR’s usual IV sits around 85% (it’s a high-vol leveraged ETH proxy: its price swings hard with Ethereum, so the payments stay fat); Gemini’s own quoted IV of 75.6% is below that, and yet it called it the bottom of the range. The figures don’t even agree with each other, which is the giveaway. A trader trusting this would sell close to the share price thinking the payments were thin, when in fact this stock pays well precisely because it swings so much. The number the trader thought they were acting on came from a tool that doesn’t know what it doesn’t know.

Where it falls short (the right answer): Pull the IV figure from your broker or Barchart. Paste it in with the share price and the date. Let the model read it the way the previous section describes (rich, normal, or thin) but the figure itself has to come from a tool that can see the live market.

Specific strike recommendations without chain data

The question: “Which price should I sell BMNR at this month?” This is the question most likely to cost an ordinary trader real money if they take the answer at face value.

Why it earns its place: Choosing the price to sell at is the most important call a covered-call seller makes. Too low and the shares get taken off you at a loss; too high and the payment isn’t worth the money you’ve tied up. An AI picking that price without live data is inventing the single most important number in the trade.

The pattern is always the same, and the Gemini example above shows it in full. The prices hang together: the one nearer the share price pays more than the one further away, just as the textbook says. They’d pass a quick glance. They match no trade you can place. They come from the model’s general sense of how these payments work, not from any live data.

The right way round is the reverse. Pull two or three candidate prices from your broker. Paste them in with the relevant details. Ask the model to weigh up your shortlist against what you’re trying to do. The model judging numbers you brought is useful. The model inventing the numbers to judge is not. Prompt 3 of the covered calls post is the working version of the right approach.

Where it falls short (the right answer): Treat any specific price the model gives you, when you haven’t shown it the live market, as fiction. Make it weigh up your shortlist instead of inventing one.

Earnings dates: it knows roughly, not exactly

The question: Does the company report results during my trade? The expected swing balloons before results and collapses after. Getting caught holding a call through an announcement you forgot about is one of the most common ways sellers get burned.

Why it earns its place: The reason it fails is built in. Models are trained on text full of past results dates, but companies move their reporting dates and the model can’t see the current calendar. Asked “does BMNR report before the June 20 expiry?”, a model can latch onto “BMNR usually reports in mid-May” from last year’s schedule, when the real date is different. It doesn’t know that it doesn’t know.

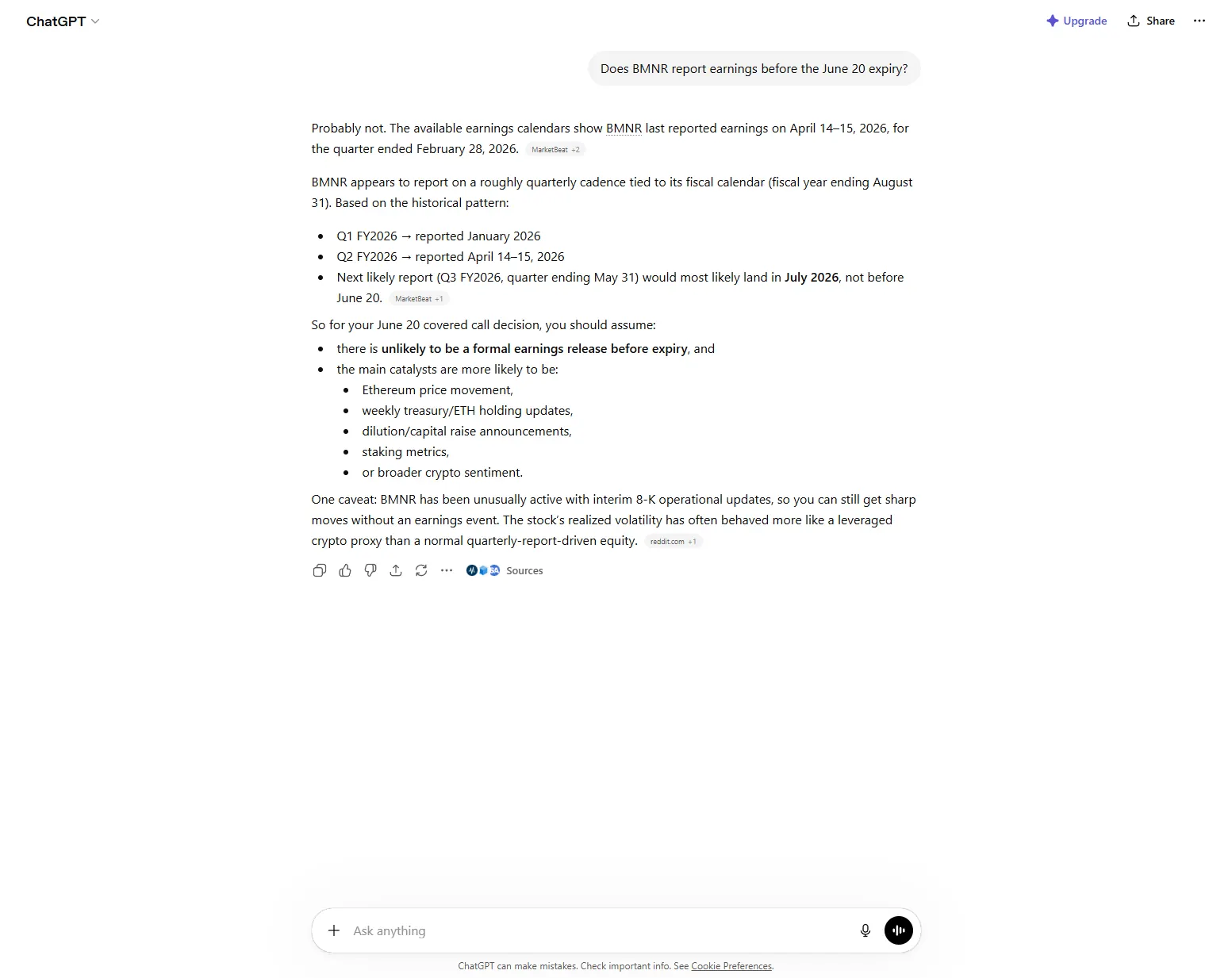

I ran this on 2026-05-16, the exact prompt, no date context given, to ChatGPT with web search on:

“Probably not. The available earnings calendars show BMNR last reported earnings on April 14–15, 2026, for the quarter ended February 28, 2026. [MarketBeat +2]

Q1 FY2026 → reported January 2026 Q2 FY2026 → reported April 14–15, 2026 Next likely report (Q3 FY2026, quarter ending May 31) would most likely land in July 2026, not before June 20.”

Web search added real-looking sources. What it didn’t add: any warning that reporting dates move, that a surprise filing could shift the timing, or that the pages it cited might lag the company’s own calendar. The confidence wasn’t earned. It was borrowed from how official the sources looked. The answer might be right. The certainty isn’t.

I treat any specific date the model gives me as something to check, not a fact. The event-window prompt is built around that: it produces the list of things I should look up, results dates among them. AI is good at the list. Confirming each one is a job for the broker or the company’s own page.

Where it falls short (the right answer): Check the company’s investor relations page, the Nasdaq calendar, or your broker’s. Use the AI to remind you what to look for, not to confirm it.

Black-Scholes calculations on hypothetical inputs

The question: “If the stock’s at $21.77, the payment is $1.50 and there are 28 days left, what’s the fair value of this option?” This is the kind of question that sounds technical enough to deserve a precise answer.

Why it earns its place: There’s a standard formula for pricing an option, Black-Scholes, and the model can write the code for it. I haven’t tested AI-written pricing code against my broker’s calculator myself. I use the broker for the numbers I trade on. But the ways it goes wrong are well documented. The same small errors creep in: most commonly, mixing up how many days are in a year, trading days (252) versus calendar days (365), which quietly shifts the answer. The result reads as precise, to several decimal places, while resting on a calculation that’s subtly off. MarketCalls.in, an independent trader site, documents this exact slip in AI-written pricing code.

A seller leaning on an AI’s pricing to judge how likely they are to get called away is getting false precision. The broker’s calculator uses the live market. The AI’s calculation uses your imagined inputs with a small formula error baked in.

Where it falls short (the right answer): For anything you’ll trade on, use the broker’s tools. Use AI to explain what a number means, not to produce the number you’ll act on.

Assignment probability without live delta

The question: “What are the chances my BMNR $23 call gets called away before June 20?”

Why it earns its place: Your broker has a number for this. There’s a quick rule of thumb behind it: a call’s delta, the figure your broker shows next to each price, roughly doubles as the chance the shares get called away, so a 0.28 delta means about a 28% chance. That shortcut needs the live delta, which moves with how close the stock is to your price and how much time is left. Without that live figure, the model can’t work it out. Asked anyway, many models will give you something that sounds like analysis. “Around 25–30% based on the stock’s history” is the classic made-up answer.

I’ve run versions of this across active BMNR trades: asking a model for the odds of getting called away before the trade ends, without giving it the live numbers. The pattern holds: a plausible figure built from a guessed-at volatility and a named formula, not from the live market. It passes a quick glance. It doesn’t match what the broker actually shows. The number that looks like a calculation is a guess.

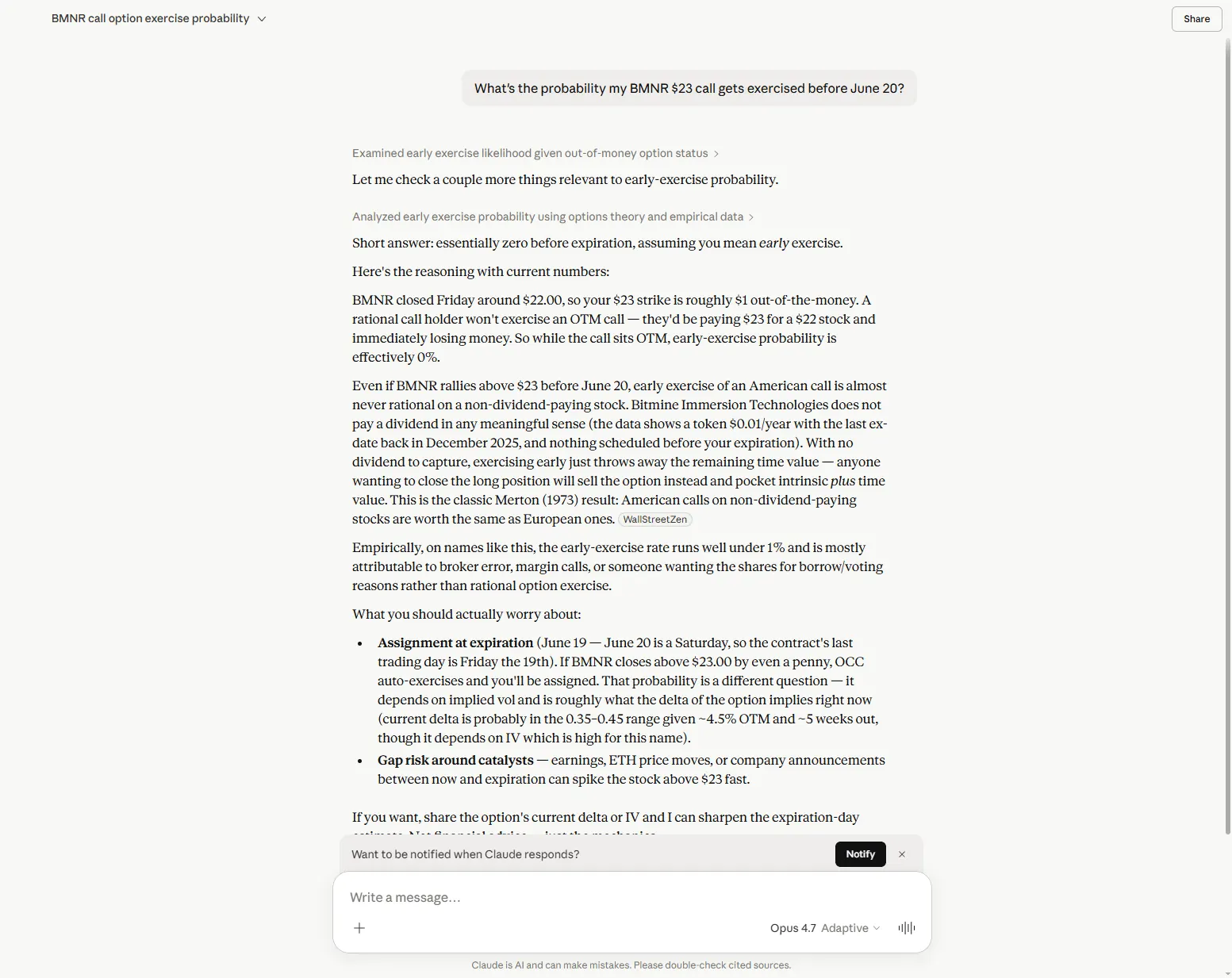

The 2026-05-16 test on Claude.ai (Opus 4.7, Max plan, web search enabled) is typical. It searched for BMNR’s price, guessed the volatility from old references, and ran its own sum:

“Plugging that into a Black-Scholes-style N(d2) calc with σ ≈ 90–110% gives a risk-neutral probability of finishing above $23 of roughly 30–40%. If you want the probability it just touches $23 at any point before expiration (relevant if you’d close the position there, not hold to expiry), that’s roughly double — call it 55–70%.”

The volatility figure of 90–110% was guessed from old references found by web search. The formula is named correctly. The answer (30–40%) looks like a calculation because it comes wrapped in a labelled method. It isn’t one: the inputs are guessed, not pulled from the live market. A different volatility guess gives a meaningfully different answer. The model didn’t have what it needed to be sure, and was sure anyway.

It’s worse for a stock like BMNR. The delta shortcut holds up on a calm stock, but BMNR moves with Ethereum and swings hard, and that makes the rough rule bend: the real odds drift away from what the simple version says, in a direction that depends on live market detail the model can’t see. So it’s not just that the model’s number is out of date; the method it’s using is the wrong one for this stock. The figure it hands you looks about right and is wrong underneath. A trader using it to decide how big to go, or whether to reshuffle, is acting on a guess dressed up as a calculation.

Where it falls short (the right answer): Your broker’s figure uses the live market. Use it for the trade. Use AI to explain what the figure means and what’s behind it, not to produce the figure itself.

Where AI for options trading helps, and where to stop

The shape across these ten items is simple enough to hold in your head.

| Part of the trade | AI useful? | When to put it down |

|---|---|---|

| Sense-checking the idea | Yes, its strongest job | Never |

| Reading the volatility figure you paste in | Yes | The moment you ask it to tell you the figure |

| Weighing up your shortlist of sell prices | Yes | The moment you ask it to invent the prices |

| Listing what to look out for | Yes | The moment it names a specific date, check it |

| Reshuffle, close, or hand over the shares | Yes, choices against your goal | When you need a live price |

| Live prices and volatility figures | No | Always: these are broker tools |

| Pricing an option from scratch | No | Always: use the broker’s calculator |

| Odds of getting called away | No | Always: that’s a live-market number |

The pattern: AI is a strong second opinion on anything it can reason through from numbers you bring it. It is a confident fabricator on anything that needs it to reach out and pull a live number it can’t see. The Prompt Stack is what holds the line, the FILTER stage especially, where you either paste the real data in or admit the model can’t do this one.

Field Report

What worked: Thinking jobs against data you bring: sense-checking the idea, naming your intent, working through the choices, reading the figures, reviewing afterwards. The four “gets it right” items are the four I run on every BMNR trade.

What didn’t: Anything that needs a live number the model can’t see: current prices, volatility figures, results dates, the odds of getting called away. It will give you a number anyway. The number will look right and won’t be.

Bottom line: These aren’t accidents, they’re built in. Gemini invented a fresh order book for me this morning, unprompted and to two decimal places, same as it does every time. At least it’s consistent.

The one rule that makes AI safe for options trading fits in a sentence: never ask it for a number it cannot see. Every useful prompt in the covered-call routine either hands the model the data or tells it plainly not to make the number up. Two companion posts show how: 7 AI prompts for covered calls maps the entry-side prompts to seven decision moments, and AI covered calls: when NOT to sell another one handles the check before you sell another one once a trade has closed. And for the exit itself, the decision to sell the shares rather than the call, the prompt I run before any sell applies the same write-it-down-first discipline. Read them next.

The three made-up answers above (Gemini’s invented options table, ChatGPT’s confidently wrong results date, Claude’s guessed-at odds) are all logged at The Lessons, alongside every other AI slip caught on this site. Worth a scan if you want to know how each tool fails before you trust it. Each one also has a named type (the invented number, the confidently-wrong fact, the borrowed certainty) in the nine named failure modes.

Ben tests which AI assistants can be trusted with a real decision, the kind where being wrong costs real money. The verdicts here are what he found, including the times a tool simply wasn’t worth the trust. About Ben →

The site runs AI on real investing decisions. Start with the Prompt Stack for the four-stage framework, or the Field Guide PDF for the condensed version, free, no email.