// On this page

Every other list of Claude prompts for investing shows you the prompts and stops. You’re meant to take it on trust that the templates work, on names you don’t know, with outputs nobody’s seen. Which is a curious way to write about not trusting AI blindly. The four lists I read while researching this post share that single tell. They give the prompts. They do not give the outputs.

This post does both. Six Claude prompts for investing, real examples of what each one returned when I ran it on MSFT, META or NVDA, and an honest note on what I still had to check before the output was usable. The names are MSFT, META and NVDA, big well-known companies where Claude has the most training data and gives the most defensible answers. Run the same prompts on a less-covered name and the output thins out with them; that’s in the closing section.

One rule ties the six together. Claude is good when you give it real text to analyse and bad when you ask it to invent. Every prompt below treats Claude as a reviewer (fed real filings, real transcripts, real news, or your own stated thesis) and asks it to find what you missed. None of them ask Claude to generate ideas, pick stocks, or predict prices from nothing. That distinction is the single prompt change that made AI analysis worth using, and it sits underneath everything below.

What’s a quick snapshot of this company?

A first pass on any name you’re considering. Business model, segment split, the risks the company itself names. The “flag anything I should verify” instruction is the bit most published prompts skip, and it’s the bit that does the work. Claude will tell you which numbers are likely stale if you ask.

I just re-ran this on MSFT (Claude Opus 4.7, 20 May 2026). The business model paragraph was tight. The segment split came back as FY2024, roughly two years behind current reporting, and the Verdict section flagged exactly that, told me Microsoft has since restructured its segments as of Q1 FY2025, and instructed me to check the live 10-K (a US company’s annual report) before quoting the percentages anywhere.

SCOPE: Work only from published sources you can name (the company’s filings and annual report, audited accounts) and anything I paste in; don’t fill gaps from memory, and say so if you can’t verify something rather than guess. Give me a factual snapshot of [COMPANY NAME] as a business, not a view on whether to buy it.

FILTER: Provide: (1) one-paragraph business model description; (2) primary revenue segments with approximate % split (use the most recent annual report you have training data on, and state the period clearly); (3) top three risks the company itself names in its most recent filing; (4) one sentence on who the main listed competitors are.

Do not generate price targets, earnings forecasts, or buy/sell recommendations. Where you are working from training data rather than a specific cited source, say so.

VERDICT: Flag any item in the above where you are uncertain of accuracy and I should verify against the live filing.

What does each side look like: bull and bear, written as separate analysts?

Before buying more of a stock you already own, force Claude to argue both sides. The instruction that makes this work isn’t “give me a balanced view”. Claude balances by default, and the result reads as mush. It’s the instruction to write the two cases as two separate analysts who each genuinely believe their case and are trying to convince a sceptical investment committee. That framing suppresses the hedging.

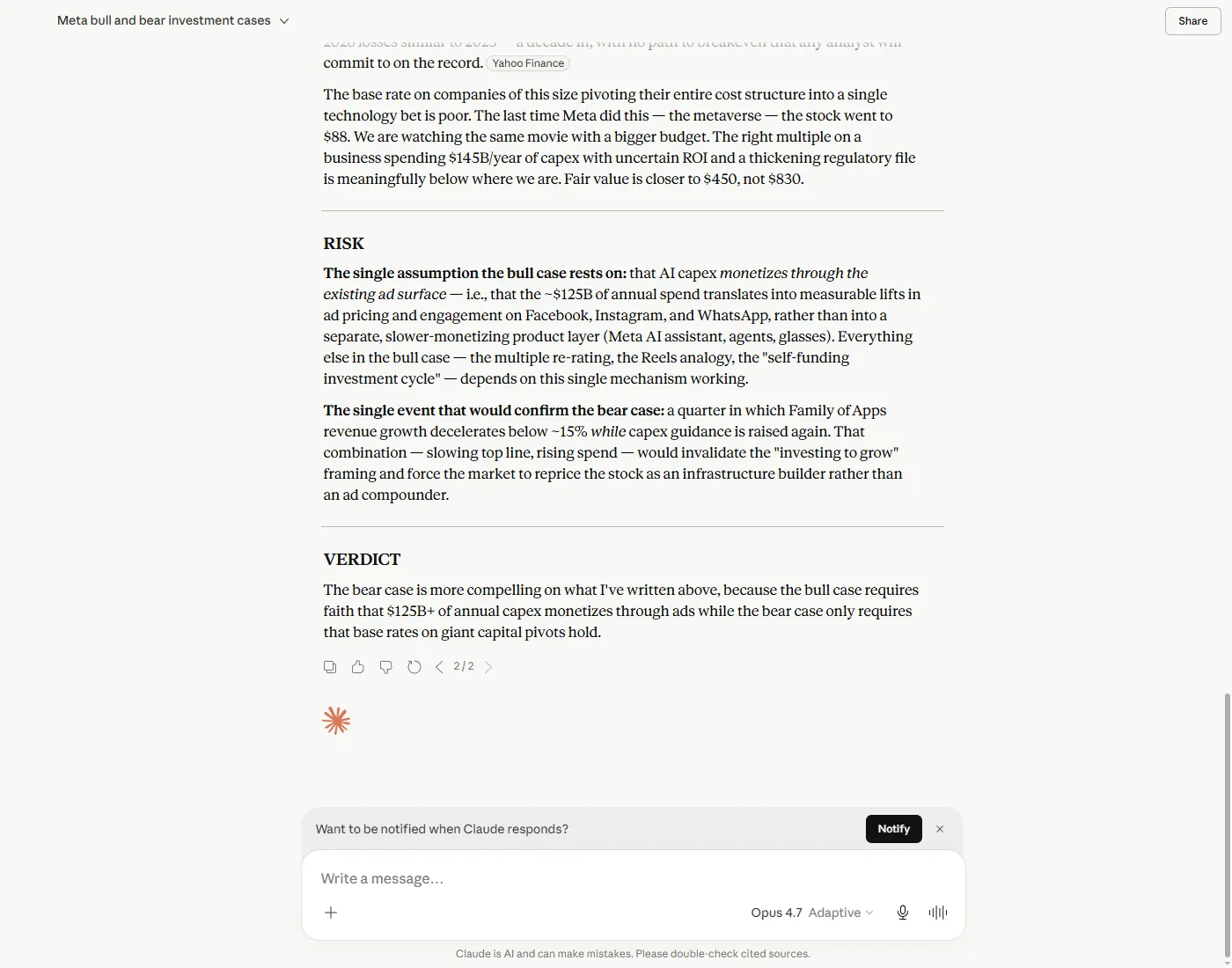

I just re-ran this on META (Claude Opus 4.7, 20 May 2026, with live search on). The bull case argued the market was mistaking a temporary capex peak (capex being the money a company spends building things like data centres, here the new $125–145B 2026 guide) for a permanent return profile. The bear case argued META is being priced like an ad company but now spends like a hyperscaler, $125B+ a year on AI infrastructure, quietly called “growth investment” without management being made to defend the framing. Claude’s own verdict at the close: the bear case is more compelling, because it only needs the base rates for giant capital programmes to hold, while the bull case requires faith that the spending pays off through the existing ad business.

I held META through the Q1 results on a version of the bull case. Reading the bear case back today, the capex-without-payback-timeline frame still applies, but the drop after earnings means I’d ask Claude a different question now (“is the bear case priced in at $606?”), not this one.

SCOPE: Work only from what you can source and name, plus anything I paste in; don’t invent figures, and flag where a claim is your inference rather than something you can verify. You will write two separate sections: a bull case and a bear case for [COMPANY NAME]. Each section should be written as if the analyst genuinely believes that position and is trying to convince a sceptical investment committee. Do not balance the two views or hedge between them.

FILTER: Bull case: make the strongest possible case for why [COMPANY NAME] could outperform over the next 2–3 years. Cover the business model, competitive position, and the specific market misunderstanding you think exists. Bear case: make the strongest possible case for why the current price is wrong. Cover the risks the bull case papers over, and the scenario where the business underperforms.

RISK: At the end, name the single assumption the bull case depends on most, and the single event that would confirm the bear case.

VERDICT: Which case do you find more compelling based only on what you’ve given me above? One sentence.

Why did the stock move, reading only the pasted context?

For when a name you own moves on news and you want to read it properly before reacting. The trap with this kind of prompt is letting Claude retrieve the news for you; it’ll narrate something plausible from training data and you won’t know it’s wrong until later. Paste the actual headline or release excerpt, and tell Claude to work from that text alone.

I just re-ran this on NVDA (Claude Opus 4.7, 20 May 2026, with the Q4 FY2026 release excerpt pasted in). The first thing Claude did was flag what I hadn’t given it, the direction of the price move, and answer all three questions conditionally on direction. If it had sold off, Claude reckoned the most likely culprit was the gross margin (the share of each pound of revenue left after the direct cost of producing it), and a non-committal China response that analysts had flagged as a known risk going in.

Here’s the catch, and it’s the whole point of the prompt. Claude’s margin read was wrong. It described a guide-down to the low-70s against a figure around 73.5%, which turned out to be the previous quarter’s number. The actual Q4 FY2026 release showed a gross margin of 75.0%, a beat, with forward guidance in the mid-70s. There was no guide-down. Claude had reached past the text I pasted and pulled a stale figure from its training data, the exact failure this prompt is built to catch, doing it inside the prompt meant to prevent it. I only knew because I checked the release against the live numbers afterwards. If you do not, the wrong figure is the one you walk away with.

The trap with this kind of prompt is letting Claude retrieve the news for you; it'll narrate something plausible from training data and you won't know it's wrong until later.

SCOPE: Work only from the news context I paste in for [COMPANY NAME]‘s move today; don’t add facts from memory, and if something you’d need isn’t here, say so rather than guess.

FILTER: [PASTE: earnings release headline / news excerpt / management statement, 2–4 paragraphs maximum]

Given only the above, explain: (1) what the likely immediate driver of the price move is; (2) what investors were expecting going in, if you can infer it from the language used; (3) whether the move looks like a sentiment reset or a fundamental revision.

Do not speculate beyond the text I’ve pasted. If you need more context to answer one of the three questions, say which question and what you’d need.

VERDICT: One sentence. Is this a move worth acting on, or one to sit with?

What do I need to verify before clicking buy?

This is the prompt I run before a discretionary buy on any name. Not asking Claude for a recommendation, asking it to list what I don’t know and should check first. The ranked three-item Verdict at the end is the bit that earns its place; it forces prioritisation rather than a dump of every theoretical risk.

I just re-ran this prompt on MSFT (Claude Opus 4.7, 20 May 2026). The first thing Claude did was call out the temporal premise: Q3 FY2026 had already reported on April 29, so “ahead of” the results was no longer accurate. From there it pivoted the entire pre-trade check onto the post-earnings drift: the 5.2% drop after a strong beat, the 67.6% gross margin (the narrowest since 2022), and the $190B 2026 capex commentary that broke the “capital-light cloud compounder” narrative for a lot of holders. The “single consensus assumption most at risk” came back as the one most worth quoting: “Microsoft’s AI capex is a capital-light, high-return investment that the strong balance sheet easily absorbs.”

The prompt template keeps the model listing what to verify before the trade, not handing you a recommendation.

When the model knows the trade window has already passed, it correctly tells you so, and the prompt does its real job, just on a different question than you intended. That's a feature, not a failure.

It also exposes a lesson worth tagging: what you remember an AI told you weeks ago is not necessarily what it would say today.

SCOPE: Work only from what I tell you below; don’t fill in figures or events from memory, and if something you’d need to check isn’t here, say so rather than assume it. I am considering [ACTION: buying / adding to / selling some of] [COMPANY NAME] before [EVENT OR DATE]. Your job is not to tell me whether to do it. It is to list everything I should know and verify before I do.

FILTER: I currently [hold / do not hold] [COMPANY NAME]. My reason for the action: [ONE SENTENCE]. What I already know: [3–5 bullet points of what you’ve already checked].

Walk me through:

- What catalyst or data point am I most likely to have missed that is relevant to this action?

- Is there an earnings release, dividend, index event, or macro date inside the next 30 days I should be aware of?

- What is the single consensus assumption about this company that is most at risk of being wrong right now?

Do not invent specific dates. Flag any date you cite as “verify this before acting.”

VERDICT: List the three most important things to check before placing this trade. Ranked by how likely they are to change my mind.

Is the earnings-call language committed or just optimistic?

After an earnings release lands, paste in the prepared remarks and ask Claude to sort the language into what management committed to versus what sounded confident but wasn’t a commitment. This is the task where Claude reliably out-reads the alternatives. When I ran the same META Q1 2026 CFO passage on Claude, ChatGPT, Perplexity and Gemini in May, Claude was the one that picked up the word “underestimate” as one-sided phrasing, the signal the three other tools missed when reading the same passage.

I just re-ran this on the META Q1 2026 prepared-remarks capex section (Claude Opus 4.7, 22 May 2026, with Zuckerberg and Susan Li’s commentary pasted in). Different passage from the May test, same task. Claude separated the numbers from the rhetoric cleanly: COMMITTED caught every figure including the precise “increased from our prior range of $115B–$135B”. OPTIMISTIC BUT UNVERIFIABLE flagged the language tell I’d missed on first read: “significant amount of AMD chips”, with Claude noting that the Broadcom clause two lines earlier had a specific number (“more than 1 GW”) and this one didn’t. Claude’s verdict: management commits hard on the audited and near-term numbers, but every statement carrying the multi-year AI thesis (returns, efficiency, strategic advantage) is unfalsifiable. The commentary anchors credibility with figures while preserving optionality on the only claims that justify the spend.

If earnings analysis is your main use of AI, the five-prompt earnings-call sequence goes deeper than this one prompt. This is the single-prompt version for everyone else.

SCOPE: Work only from the management commentary I paste below; don’t bring in outside facts from memory, and say so if the text doesn’t show something rather than fill it in. You are checking whether the prepared remarks reflect genuine confidence or performative confidence.

FILTER: Below is the management commentary section from [COMPANY NAME]‘s [QUARTER] results.

[PASTE PREPARED REMARKS: management commentary only, 3–8 paragraphs]

Produce two short lists:

- COMMITTED: statements with a specific number, specific timeline, or falsifiable claim

- OPTIMISTIC BUT UNVERIFIABLE: statements that sound positive but contain no specific number, timeline, or measurable commitment

RISK: For the single most important line in the commentary, the one investors will remember, classify it as COMMITTED or OPTIMISTIC BUT UNVERIFIABLE, and state your reasoning.

VERDICT: One sentence. Does this commentary commit management to anything specific, or does it preserve their optionality?

Where are the holes in my thesis?

You’ve already got a view. Force Claude to find the weakest assumptions inside it before you act on it. The Prompt Stack in its most stripped-down form: one prompt, one second opinion, no sympathy. The “do not praise what’s sound” instruction is what makes this work. Without it, Claude leads with what your thesis gets right, and the critique gets buried.

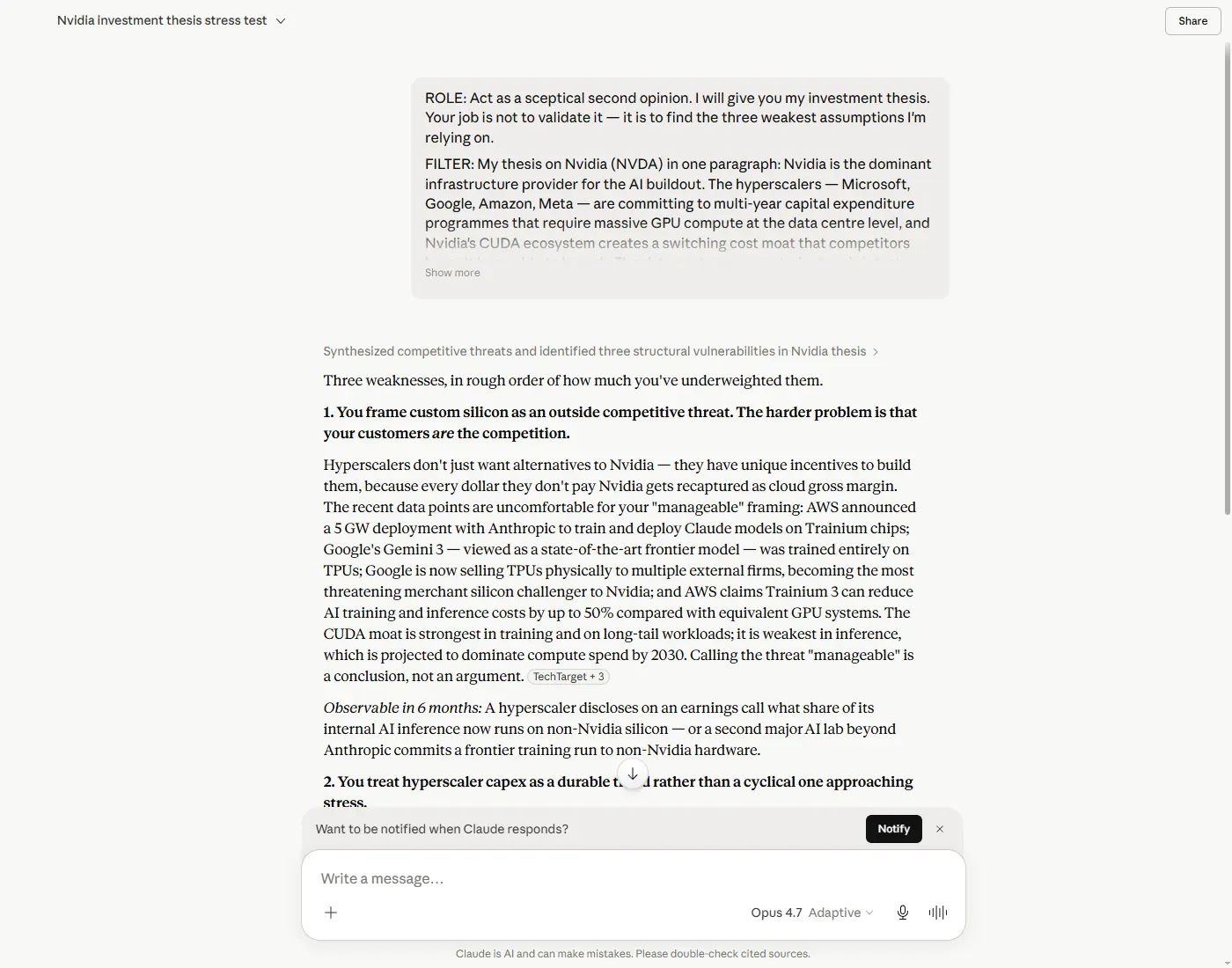

I just re-ran this on a stated NVDA thesis (Claude Opus 4.7, 20 May 2026, live search on). I don’t hold NVDA. The thesis was built as a stress-test exercise, the kind a data-centre bull might construct, because that’s where AI-bull blind spots concentrate. Claude named three weaknesses the thesis was understating. The first: it framed custom silicon as an outside threat, when NVDA’s own customers (Anthropic on Trainium, Google selling its TPU chips to others) are now the competition. The second: the big four buyers spending on AI infrastructure were being treated as a durable trend, when their spending as a share of revenue (Claude’s own rough figures put it near 46% at Alphabet, 47% at Microsoft, 54% at Meta and 86% at Oracle) sits at levels with no real precedent. One spending cut from any of them could reprice the whole sector. The third: the thesis’s load-bearing claim (“compound earnings at rates that justify the price”) was stated without doing the maths on what the share price already reflects. Claude’s own one-sentence verdict: the second weakness, the infrastructure spending, is the one most likely to matter in the next twelve months.

SCOPE: Work only from the thesis I paste below; don’t bring in facts or figures from memory, and if something you’d need to judge it isn’t here, say so rather than assume it. Your job is not to validate the thesis. It is to find the three weakest assumptions I’m relying on.

FILTER: My thesis on [COMPANY NAME] in one paragraph: [PASTE YOUR THESIS].

Do not praise what’s sound in the thesis. Focus only on the parts that are: (a) assumptions I’m stating as facts, (b) things I’d need to be true but haven’t verified, or (c) risks I appear to have discounted.

RISK: For each of the three weaknesses you identify, name one observable event in the next 6 months that would confirm the risk is real.

VERDICT: Which of the three weaknesses is most likely to matter in the next 12 months? One sentence.

Where these Claude investing prompts fall short

Three honest limits apply to the whole list.

Claude’s training data is stale by design. Any specific number it states (segment splits, capex figures, consensus expectations, dates) is from training data that may be six to twelve months behind. I noticed this twice in the runs above: when I re-ran Prompt 1 on MSFT, the segment split came back as FY2024 (two years stale); when I re-ran Prompt 4, Claude flagged that Q3 FY2026 had already reported. The “flag what’s uncertain” instruction works in both cases, but Claude doesn’t always know what it doesn’t know, so verify any number you’d act on against the company’s investor relations page, the live earnings calendar, or a real consensus source.

Output quality is uneven by ticker. AAPL, MSFT, META, NVDA: well-covered, dense training data, defensible answers. Less-covered names (UK AIM stocks, smaller US listings, anything outside the S&P 500) get thinner, more hedged outputs. The prompts still work; the verification load goes up.

None of these prompts give you live data. Claude reads what you paste in or what’s in its training. For live numbers, the tool comparison post covers which model to use for retrieval. That’s a different job from the one above. The same boundary runs through options work, where the cost of forgetting it is steeper: what AI gets wrong about options trading is the line between a number Claude can reason about and one it will invent. The documented failure cases, where one of these tools invented data rather than flagging the gap, are on the lessons page.

The discipline running through all six prompts is the same.

Claude is a reviewer, not an oracle. Feed it real text and it's the best language analyst I've tested. Ask it to generate research from nothing and you'll get plausible-sounding noise.

Pick the prompt that fits the decision you’re making, give it real material to work with, and verify anything you’d act on. The Prompt Stack is the longer version of that rule.

Field Report

What worked: Six prompts that each treat Claude as a reviewer of real material (pasted text, a stated thesis, a named company), not an idea generator. Each one earned its place on a real decision on MSFT, META or NVDA.

What didn’t: None of these prompts gives you live data, current consensus figures, or anything Claude’s training doesn’t already hold. Output thins out on less-covered names. The “flag what’s uncertain” instruction works but isn’t a substitute for checking the investor relations page.

Bottom line: Useful on the names Claude has training data on, used as a reviewer rather than a generator. The verification work is on you. These prompts shorten the read, not the check.

Ben tests how far you can trust the main AI assistants, and publishes exactly where they get things wrong. Every post here is a first-hand test with the receipts, including the times a tool simply wasn’t worth the trust. About Ben →

The site runs AI on real investing decisions. Start with the Prompt Stack for the four-stage framework, free and ungated, or the Bluff Filter for the paste-ready version with a real before and after.